What Can Be Seen as Indirect Inheritance (Estate) Tax in Canada?

While Canada does not impose a formal inheritance tax like some other countries, there are several mechanisms that can effectively function as indirect estate or inheritance taxes. These mechanisms impact the value of an estate or the assets received by beneficiaries. Below is a breakdown of the main indirect taxes or fees that arise upon death:

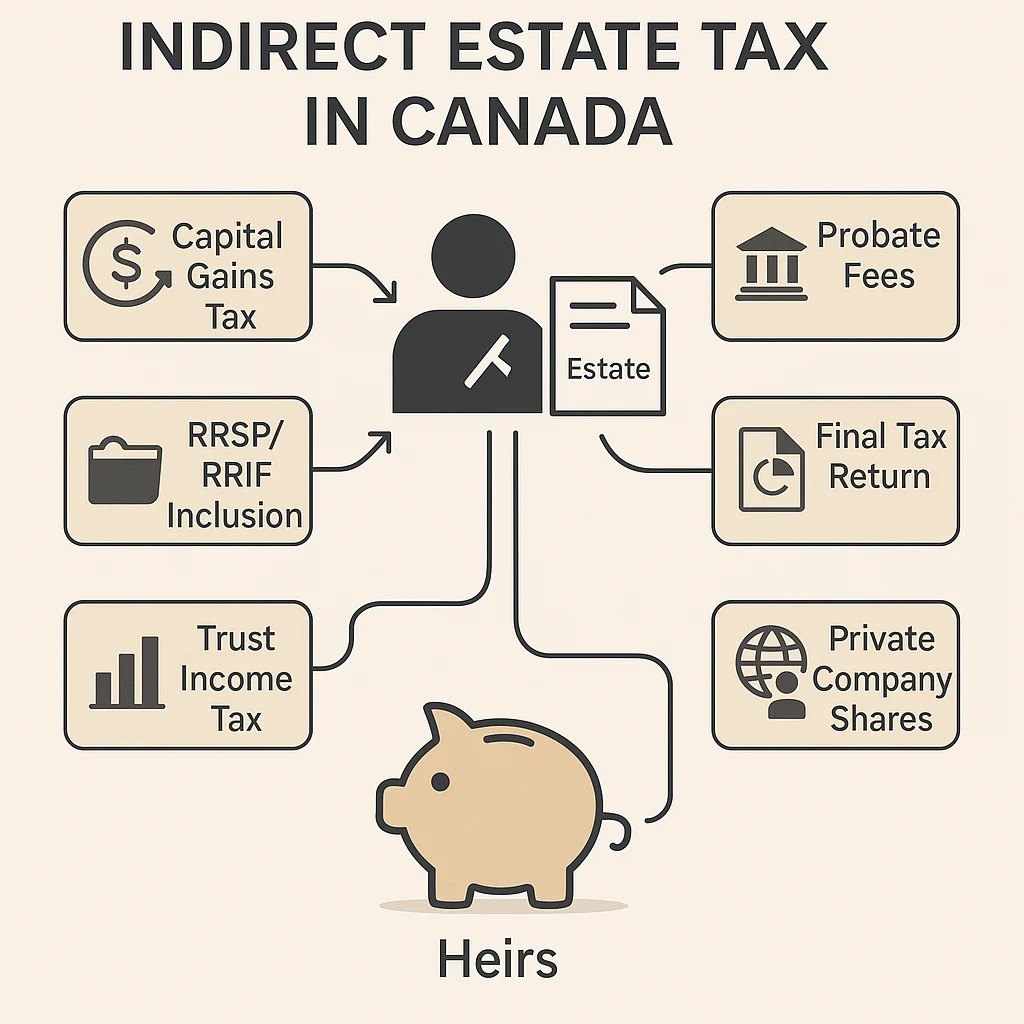

- Deemed Disposition of Assets at Death

Upon death, individuals are considered to have sold all their capital property at fair market value, which may trigger capital gains tax. This is one of the most significant tax events at death in Canada. - Tax on Registered Accounts (RRSP/RRIF)

If a Registered Retirement Savings Plan (RRSP) or a Registered Retirement Income Fund (RRIF) is not rolled over to a spouse or dependent child, its full value is included as income on the final tax return of the deceased. - Probate Fees (Estate Administration Tax)

In provinces like Ontario and British Columbia, probate fees are charged based on the estate’s value. Though not technically a tax on inheritance, they reduce the value passed on to beneficiaries. - Final Income Tax Return

The deceased’s final tax return may include employment income, investment income, and other taxable gains, which may significantly reduce the estate’s net value. - Trust Income Tax (if Estate becomes a Trust)

If an estate remains open and earns income before distribution, it may be taxed at graduated or flat trust tax rates, depending on the circumstances. - Non-Resident Beneficiaries

If beneficiaries reside outside Canada, there may be withholding taxes or complications with foreign tax credits that can indirectly affect the estate. - Tax on Private Corporation Shares

Valuation and potential capital gains on deemed disposition of shares in a private company can have significant tax consequences at death.

Although Canada does not impose a direct inheritance tax, the combined impact of capital gains, income inclusion from registered plans, probate fees, and other taxes can reduce the amount ultimately inherited. These financial consequences function similarly to an inheritance tax and should be carefully planned for to minimize their effect on heirs.

Allen Madelin Avocats offer consultations both in person and via videoconference. The first consultation is offered for $125. For more information, please contact us by telephone: 1 514 904 4017 or by e-mail: [email protected].